Content Courtesy Dimensional Fund Advisors. DFA Authors: John Morrison, CFA Senior Investment Strategist and Vice President | Matt Lipps, CFA Associate Investment Strategist. See the DFA article PDF here.

KEY TAKEAWAYS

As in 2021, small cap growth companies with low profits drove the underperformance of small caps in Q1 2022.

Small cap companies that have had extreme balance sheet growth were also a drag on returns.

An approach that excludes small cap growth companies with low profitability and small caps with high asset growth may increase returns.

In February, we examined the underperformance of US small cap companies and pinned the lion’s share of blame for that underperformance on stocks with high relative prices (growth stocks) and low, or negative, profits. With the tumultuous first quarter of 2022 behind us, we check in on these stocks to see if it was “just a phase.”

Exhibit 1 revisits the top five detractors to the Russell 2000 Index’s performance in 2021. At the beginning of the year, these companies shared common traits: negative profits over the previous year and price-to-book ratios that placed them in the highest-relative-price quartile of the market. Stocks with high relative prices and low profitability were a poor-performing segment among small caps in 2021, and those expecting a rebound for these names were disappointed: The biggest losers in 2021 flunked the first quarter of 2022 as well.

EXHIBIT 1

Class Clowns

2021’s top detractors in Russell 2000 Index, then and now

Past performance is not a guarantee of future results. Returns are computed from the Russell 2000 Index’s published security weights and Dimensional-computed security returns. This information should not be considered a recommendation to buy or sell a particular security. Named securities may be held in accounts managed by Dimensional. The securities identified do not represent all securities purchased or sold for client accounts. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes.

At the beginning of 2022, all five stocks continued to show low profitability or high relative prices, if not both. Appian, TG Therapeutics Inc., and BridgeBio Pharma Inc. each started 2021 and 2022 in the same market segment: high relative price with low profitability. Negative profitability businesses often prop up their operations by raising equity capital. Invitae Corporation raised $1 billion from Softbank Group and therefore was also classified as a “high asset growth” name. Historically, companies with high asset growth have underperformed their counterparts with more stable balance sheets. The share price of Allakos Inc., the top detractor to the Russell 2000 last year, fell so far in 2021 that it became a value stock in 2022, though its low profitability continues to portend lower expected returns.

Rather than continue to pick on the five horsemen of the small-pocalypse, we can examine the groups of small caps with high relative prices and low profitability, as well as those with high asset growth. Exhibit 2 shows that US small caps with high relative prices and low profitability or high asset growth dragged in the first quarter of 2022, falling by a respective 12% and 20% and compounding losses from 2021. Simultaneously, small stocks with low relative prices (value stocks) and higher profitability showed positive returns amid declines in other small caps.

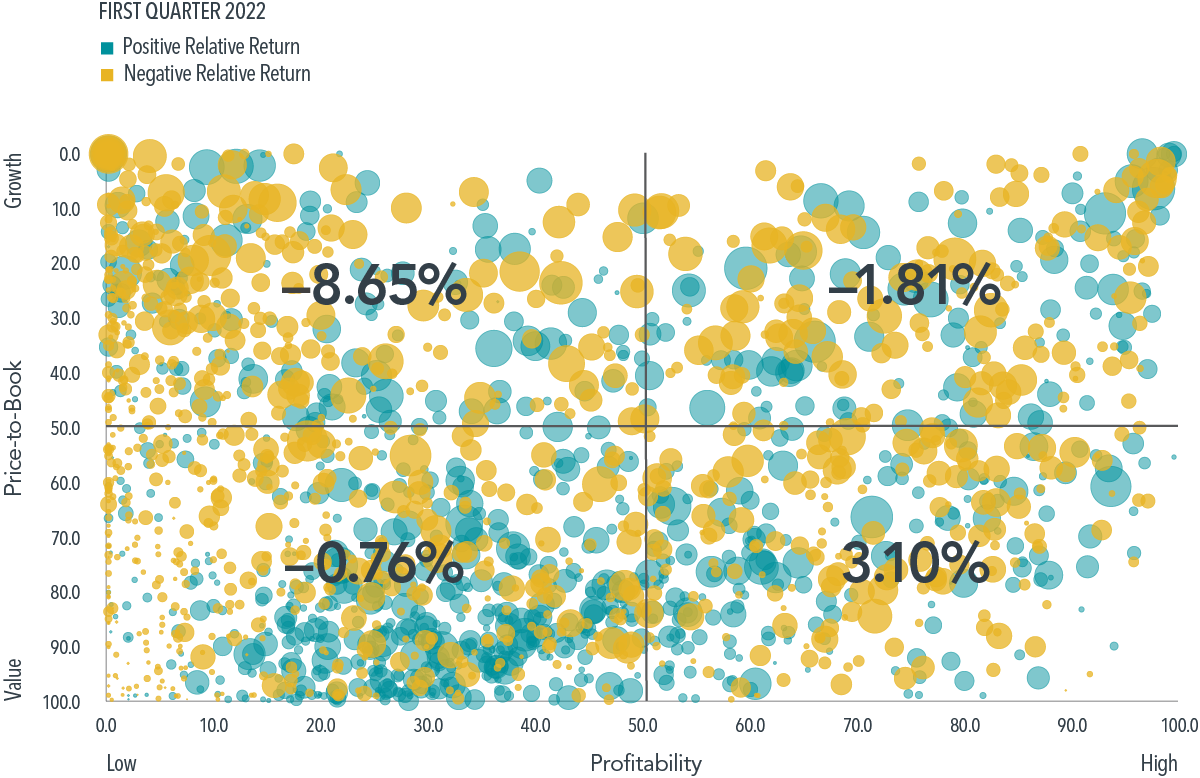

Exhibit 3 maps the Russell 2000 Index holdings on valuation and profitability characteristics and plots each company with a bubble whose size corresponds to its weight in the index; names that outperformed the index are blue, and those that underperformed are yellow. The map also overlays each quadrant’s performance and shows that a clique of growthy and low profitability names were among those underperforming the Russell 2000 for the quarter, negatively impacting the small cap index’s overall return.

EXHIBIT 2

Report Card

Returns of Russell 2000 Index and small cap market segments

Past performance, including hypothetical performance, is not a guarantee of future results. Market segment returns are the return to small caps with the stated characteristic within the Russell 2000 Index. Small cap is defined as the smallest 10% of market cap. High Relative Price, Low Profitability consists of the stocks with the highest relative prices and lowest profitability within small caps. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. High Asset Growth consists of the stocks with the highest asset growth within small caps. Asset growth is defined as change in total assets from the prior fiscal year to current fiscal year. Low Relative Price, High Profitability represents small caps in the 35% of market cap with the lowest price-to-book ratios and excludes the lowest 10% of market capitalization by profitability. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes.

EXHIBIT 3

Progress Report

Russell 2000 Index holdings, market cap percentiles, and performance relative to index

Holdings as of December 31, 2021. Stocks are plotted on price-to-book and profitability. The size of the bubble is proportional to the market capitalization of the stock. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Where book values are negative, stocks are plotted at the far left of the horizontal axis. Returns to market segments are computed from the Russell 2000 Index’s published security weights and Dimensional-computed security returns. Relative price (e.g., value and growth) designations are based on price-to-book ratios. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes.

Looking broadly across decades of returns in global markets, we observe that small cap growth stocks with low profitability or high asset growth tend to underperform over the long run. And for good reason: from the perspective of valuation theory, paying a lot for a company that earns little profit or requires frequent investment is a good sign of a low discount rate, and therefore a low expected return. By comparison, paying less for more profit indicates a higher discount rate and expected return.

In 2022, the biggest losers from 2021 continued to struggle while value names with higher profits delivered—again. Trying to pick a handful of winners from thousands of small cap companies is a recipe for disappointment. Instead, buying the small cap market minus the riffraff can improve expected returns while still allowing investors to maintain a well-diversified portfolio. Without a crystal ball to name standout performers, history and valuation theory are our best guide. We expect investors who focus on paying less (lower relative price - “value”) and getting more (higher profitability) to thrive.

DISCLOSURES

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

This information is not meant to constitute investment advice, a recommendation of any securities product or investment strategy (including account type), or an offer of any services or products for sale, nor is it intended to provide a sufficient basis on which to make an investment decision. Investors should consult with a financial professional regarding their individual circumstances before making investment decisions.

Risks include loss of principal and fluctuating value. Investment value will fluctuate, and shares, when redeemed, may be worth more or less than original cost. Small cap investments are subject to greater volatility than those in other asset categories.

Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value

Dimensional Fund Advisors does not have any bank affiliates.